In today’s fast-paced financial world, owning expensive products or accessing essential services has become much easier than in the past. One of the main reasons behind this convenience is the EMI system, which allows individuals to purchase high-value items without paying the full amount upfront. EMI stands for Equated Monthly Installment, a structured repayment method widely used in loans, credit cards, and consumer financing.

From smartphones and laptops to cars, homes, and even medical treatments, EMI has become an integral part of modern financial planning. This system not only makes purchases more affordable but also helps people manage their cash flow effectively. In this article, we will explore the EMI system in detail, covering how it works, its benefits, types, calculation methods, advantages, risks, and best practices for using it wisely.

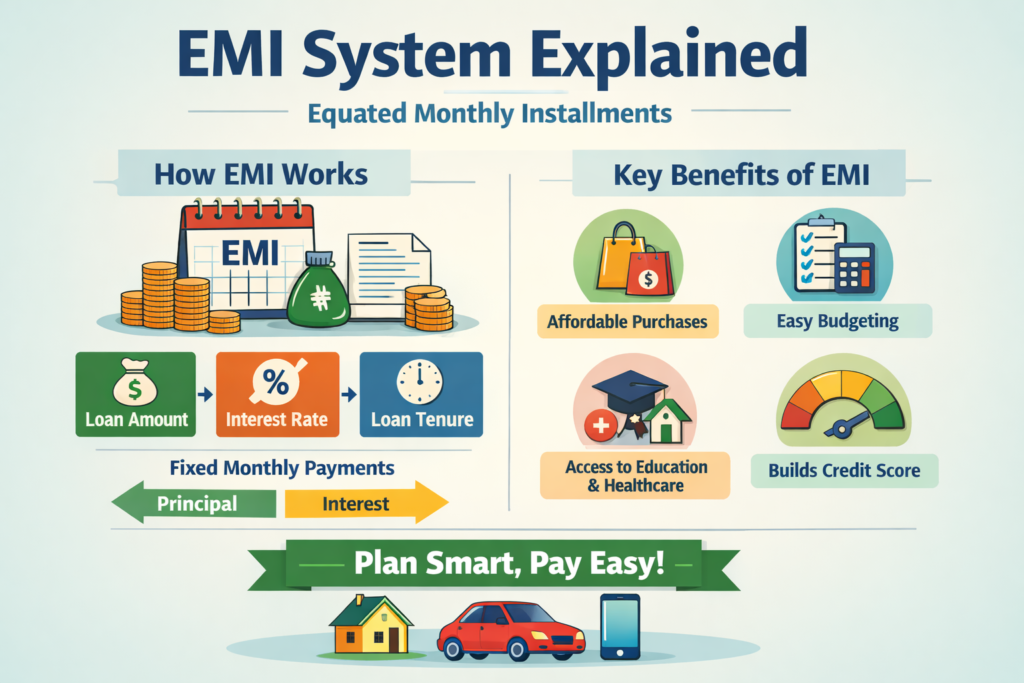

What Is an EMI System?

The EMI system is a financial arrangement where a borrower repays a loan in fixed monthly installments over a predetermined period. Each EMI payment includes two components:

- Principal amount – the original loan amount borrowed

- Interest amount – the cost charged by the lender for providing the loan

Instead of paying a lump sum, borrowers divide the total repayment into manageable monthly payments. This makes large purchases financially accessible to middle-income and even lower-income individuals.

Banks, non-banking financial companies (NBFCs), digital lenders, and retailers commonly offer EMI facilities. The system is widely used in personal loans, home loans, car loans, education loans, and consumer durable financing.

How Does the EMI System Work?

When a person takes a loan, the lender calculates the total repayment amount based on three key factors:

- Loan amount

- Interest rate

- Tenure (repayment period)

Using a mathematical formula, the lender determines a fixed monthly installment that remains constant throughout the loan tenure. Even though the EMI amount stays the same, the proportion of principal and interest changes over time.

In the initial months, a larger portion of the EMI goes toward interest, while a smaller portion reduces the principal. As time passes, the interest component decreases, and more money goes toward repaying the principal.

Types of EMI Systems

Different types of EMI options are available based on the lender, loan type, and borrower’s financial situation. Some of the most common types include:

1. Bank EMI

Banks offer EMI options on personal loans, home loans, car loans, and credit cards. These usually come with lower interest rates but require proper documentation and eligibility checks.

2. No-Cost EMI

In this model, retailers or brands absorb the interest cost, allowing customers to pay only the product price in installments. However, hidden processing fees may apply.

3. Credit Card EMI

Many banks convert credit card purchases into EMIs. This is popular for online shopping and big-ticket items like electronics.

4. Merchant EMI

Retailers partner with lenders to provide instant EMI at the point of sale. This is common in stores selling gadgets, appliances, and furniture.

5. Digital EMI

Fintech platforms offer instant EMI through mobile apps with minimal paperwork and quick approvals.

Benefits of the EMI System

The EMI system provides several advantages to consumers and businesses alike.

1. Affordability

EMI allows people to buy expensive items without financial stress by spreading payments over time.

2. Better Financial Planning

Since EMIs are fixed, individuals can budget their monthly expenses more effectively.

3. Access to Essential Services

EMI enables access to education, healthcare, and housing, improving overall quality of life.

4. Boosts Consumer Spending

Retailers benefit from higher sales as EMI encourages customers to make purchases they might otherwise postpone.

5. Builds Credit Score

Timely EMI payments help individuals build a strong credit history, improving future loan eligibility.

How Is EMI Calculated?

The EMI is calculated using a standard formula:

EMI = [P × R × (1+R)^N] / [(1+R)^N – 1]

Where:

- P = Principal loan amount

- R = Monthly interest rate

- N = Number of months

Most banks and lenders provide online EMI calculators that simplify this process. Borrowers can enter loan details and instantly see their monthly payments.

Factors Affecting EMI Amount

Several factors influence how much EMI a borrower has to pay.

1. Loan Amount

Higher loan amounts result in higher EMIs.

2. Interest Rate

Lower interest rates reduce EMI payments.

3. Loan Tenure

Longer tenures reduce monthly EMI but increase total interest paid.

4. Type of Interest (Fixed vs Floating)

Fixed interest rates keep EMI constant, while floating rates may change over time.

EMI vs Full Payment

Many consumers wonder whether EMI is better than paying in full. The answer depends on individual financial circumstances.

When EMI Is Good

- When cash flow is limited

- When no-cost EMI is available

- When the purchase is necessary

When Full Payment Is Better

- When you can afford it comfortably

- When EMI includes high interest or fees

Risks and Drawbacks of EMI

While EMI offers convenience, it also has some risks.

1. Overborrowing

Easy EMI availability can lead to unnecessary spending.

2. Interest Burden

Long-term EMIs increase total repayment cost.

3. Late Payment Penalties

Missing EMI payments can lead to fines and credit score damage.

4. Debt Trap

Multiple EMIs can create financial stress if not managed properly.

Smart Tips for Using EMI Wisely

To make the best use of the EMI system, follow these tips:

- Compare interest rates before choosing a lender

- Avoid unnecessary purchases

- Choose shorter tenures if possible

- Read terms and conditions carefully

- Maintain a good credit score

- Use EMI only for essential or high-value items

Role of EMI in Digital Economy

With the rise of e-commerce and fintech, EMI has become even more popular. Online platforms offer instant EMI options at checkout, making shopping more convenient than ever.

Buy Now, Pay Later (BNPL) models have further expanded EMI accessibility, allowing users to split payments into small installments without traditional bank involvement.

EMI in Different Sectors

1. Education

Many students use EMI-based education loans to fund their studies.

2. Healthcare

Hospitals now offer EMI for medical treatments and surgeries.

3. Real Estate

Homebuyers rely heavily on EMI-based home loans.

4. Automobiles

Car buyers commonly use EMI financing.

5. Consumer Electronics

Smartphones, TVs, and laptops are widely purchased through EMI.

Future of EMI System

The EMI system is expected to grow rapidly due to digital transformation and financial inclusion initiatives. Artificial intelligence, blockchain, and open banking may further streamline EMI approvals and repayments.

More flexible repayment plans, personalized interest rates, and instant loan approvals will likely shape the future of EMI financing.

Conclusion

The EMI system has revolutionized modern finance by making expensive purchases more accessible and manageable. It empowers consumers, supports businesses, and drives economic growth. However, responsible usage is key to avoiding financial stress.

By understanding how EMI works, comparing options, and maintaining disciplined spending habits, individuals can make the most of this powerful financial tool. Whether for education, healthcare, housing, or lifestyle purchases, EMI remains one of the most important innovations in personal finance today.