Saving money safely while earning predictable returns is a priority for many individuals. Among the most popular traditional saving options are Fixed Deposit vs Recurring Deposit (RD). Both are offered by banks and financial institutions and are known for stability, low risk, and guaranteed returns. However, many people find it difficult to decide which option suits them better.

While fixed deposits are ideal for investing a lump sum, recurring deposits are designed for disciplined monthly savings. Understanding the differences between FD and RD helps individuals choose the right option based on income pattern, financial goals, and time horizon.

This article explains what fixed deposits and recurring deposits are, how they work, their advantages and limitations, and which option may be better for different types of savers.

What Is a Fixed Deposit?

A Fixed Deposit (FD) is a financial instrument where a person deposits a lump sum amount with a bank or financial institution for a fixed period at a predetermined interest rate. The money remains locked in for the chosen tenure, and interest is paid either periodically or at maturity.

Fixed deposits are considered one of the safest investment options because returns are known in advance and are not affected by market fluctuations. Fixed Deposit vs Recurring Deposit

How Fixed Deposit Works

The working of a fixed deposit is simple:

- A lump sum amount is deposited

- A fixed tenure is selected

- The bank offers a fixed interest rate

- Interest accumulates over time

- The maturity amount is paid at the end of the tenure

Premature withdrawal may be allowed, but it often comes with a penalty.

What Is a Recurring Deposit?

A Recurring Deposit (RD) is a savings option where a fixed amount is deposited every month for a chosen period. Instead of investing a large sum at once, loans, RD encourages regular saving by allowing individuals to deposit small amounts consistently. Fixed Deposit vs Recurring Deposit

Recurring deposits are ideal for salaried individuals or anyone who prefers disciplined savings.

How Recurring Deposit Works

The RD process works as follows:

- A fixed monthly deposit amount is chosen

- The deposit is made every month

- A fixed tenure is selected

- Interest is calculated on monthly deposits

- A lump sum is received at maturity

Missed deposits may attract penalties depending on bank policies.

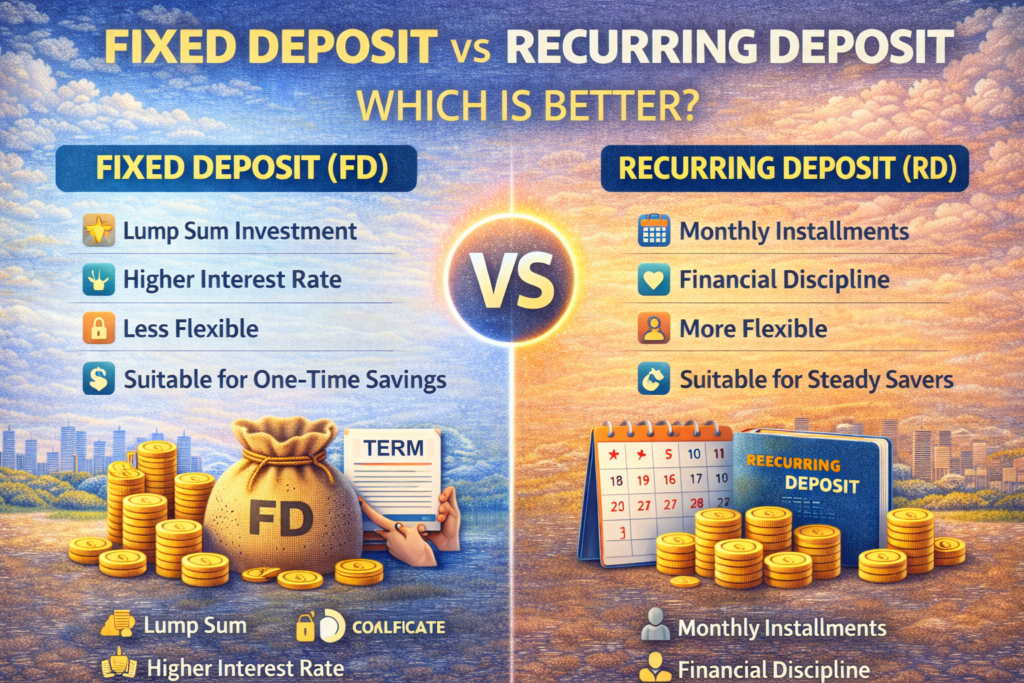

Key Differences Between Fixed Deposit and Recurring Deposit

Understanding the basic differences helps in better decision-making.

| Aspect | Fixed Deposit (FD) | Recurring Deposit (RD) |

|---|---|---|

| Investment Style | Lump sum | Monthly installments |

| Ideal For | One-time savings | Regular income earners |

| Interest Rate | Generally higher | Slightly lower |

| Flexibility | Less flexible | More flexible |

| Risk Level | Very low | Very low |

Both options are safe, but their suitability depends on saving habits.

Interest Rates: FD vs RD

Interest rates play a major role in deciding between FD and RD.

Fixed Deposit Interest

- Usually higher than savings accounts

- Fixed at the time of deposit

- Varies based on tenure and bank

Recurring Deposit Interest

- Comparable to FD rates

- Calculated on monthly contributions

- Depends on tenure and deposit frequency

Interest rates may vary from one bank to another.

Tenure Options

Both FD and RD offer flexible tenure options.

Fixed Deposit Tenure

- Short-term: a few months

- Long-term: several years

Recurring Deposit Tenure

- Usually starts from 6 months

- Can go up to several years

Choosing the right tenure helps align savings with goals.

Liquidity and Premature Withdrawal

Liquidity refers to how easily funds can be accessed.

Fixed Deposit Liquidity

- Premature withdrawal allowed

- Penalty may apply

- Partial withdrawal may not be allowed

Recurring Deposit Liquidity

- Early closure possible

- Missed installments may attract charges

- Generally more flexible than FD

Liquidity needs should be considered before investing.

Taxation (General Overview)

Tax rules vary by country, but generally:

- Interest earned on FD is taxable

- Interest earned on RD is also taxable

- Tax may be deducted at source in some cases

Always check local tax laws before investing.

Fixed Deposit: Advantages

Fixed deposits offer several benefits:

- Guaranteed returns

- Low risk

- Suitable for lump sum investment

- Simple and easy to understand

- Ideal for conservative investors

FDs are widely trusted for capital protection.

Fixed Deposit: Limitations

Despite their safety, FDs have some limitations:

- Lower returns compared to market-linked options

- Less flexibility

- Penalties on premature withdrawal

They may not beat inflation over the long term.

Recurring Deposit: Advantages

Recurring deposits encourage regular savings.

- Promotes financial discipline

- Affordable monthly contributions

- Low risk

- Suitable for small savers

- Predictable maturity amount

RDs are excellent for short- to medium-term goals.

Recurring Deposit: Limitations

Some limitations of RDs include:

- Lower returns compared to FD in some cases

- Penalties for missed payments

- Not suitable for large lump sum investment

Consistency is key for RD success.

FD vs RD: Which Is Better for You?

There is no universal answer—it depends on individual needs.

Choose Fixed Deposit If:

- You have a lump sum amount

- You want higher interest rates

- You prefer minimal involvement

- You want capital protection

Choose Recurring Deposit If:

- You earn a regular monthly income

- You want to build savings gradually

- You prefer disciplined saving

- You have short-term financial goals

FD or RD for Different Financial Goals

Emergency Fund

FD is often preferred due to quick availability of funds.

Short-Term Goals

RD is suitable for goals like vacations or planned purchases.

Retirement Savings

FDs can provide stable post-retirement income.

First-Time Savers

RD is ideal for beginners developing a savings habit.

FD vs RD: Risk and Safety

Both FD and RD are considered low-risk options.

- Returns are not market-linked

- Capital is protected

- Suitable for conservative investors

Safety depends on choosing reliable financial institutions.

Can FD and RD Be Used Together?

Yes, many individuals use both options.

Benefits of Using Both

- Balanced savings approach

- Liquidity through FD

- Discipline through RD

Combining both can help achieve multiple financial goals.

Common Mistakes to Avoid

- Ignoring liquidity needs

- Choosing very long tenure without planning

- Not comparing interest rates

- Missing RD installments

Fixed Deposit vs Recurring Deposit Avoiding these mistakes improves savings efficiency.

Frequently Asked Questions (FAQs)

Is FD safer than RD?

Both are equally safe when offered by reliable institutions.

Can RD be converted into FD?

Some banks allow conversion under certain conditions.

Which gives better returns?

FD usually offers slightly higher returns for lump sums.

Are FD and RD suitable for beginners?

Yes, both are beginner-friendly options.

Conclusion

Fixed deposits and recurring deposits are reliable and low-risk saving options suitable for different financial needs. While fixed deposits are ideal for investing a lump sum with guaranteed returns, recurring deposits are best for individuals who want to save small amounts regularly and build financial discipline. Fixed Deposit vs Recurring Deposit

Choosing between FD and RD depends on income pattern, savings capacity, and financial goals. In many cases, using both options together provides a balanced and effective approach to saving money safely.

Disclaimer

This article Fixed Deposit vs Recurring Deposit is for informational and educational purposes only. Interest rates, tax rules, and deposit terms vary by bank and region. Always refer to official bank information before investing.