The banking system in Pakistan plays a vital role in supporting the country’s economy, financial stability, and development. Banks in Pakistan provide essential services such as savings facilities, loans, payment systems, and trade finance to individuals, businesses, and the government. Over the years, the banking sector has evolved significantly, becoming more regulated, technology-driven, and customer-focused.

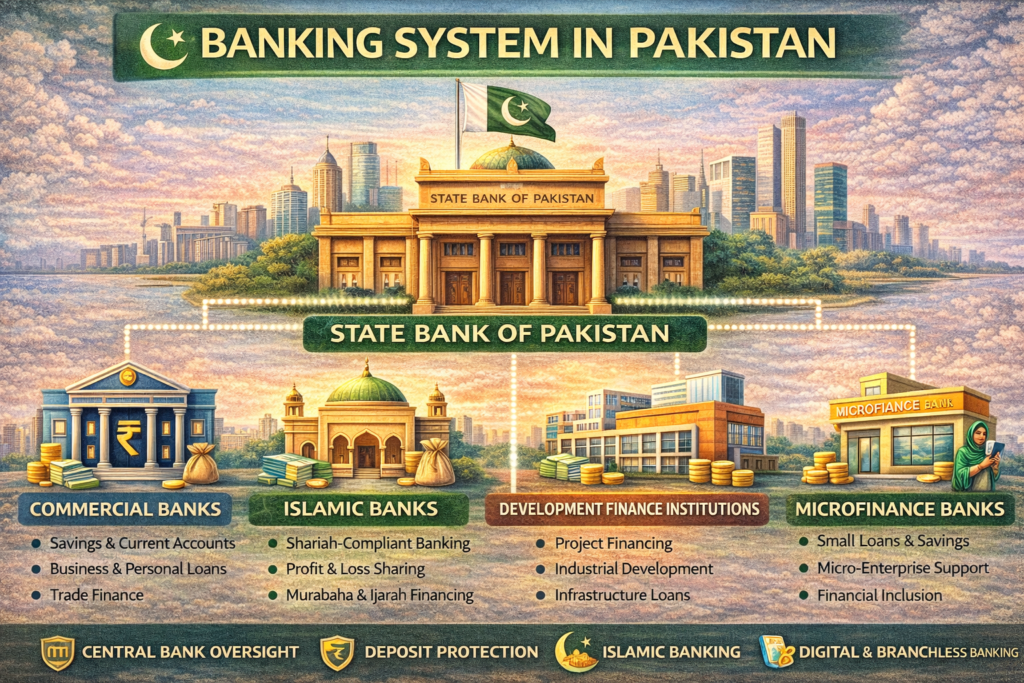

Pakistan’s banking system operates under a structured framework supervised by the State Bank of Pakistan (SBP). It includes commercial banks, Islamic banks, development finance institutions, and microfinance banks, each serving different segments of society. This diversity helps promote financial inclusion and economic growth.

This article explains the banking system in Pakistan, its structure, types of banks, regulatory framework, and its importance to the economy.

Overview of the Banking System in Pakistan

The banking system in Pakistan is a well-regulated and mixed financial system consisting of conventional and Islamic banking institutions. It supports both urban and rural populations and plays a key role in mobilizing savings and providing credit.

Key characteristics of Pakistan’s banking system include:

- Strong central bank oversight

- Growing Islamic banking sector

- Expansion of digital and branchless banking

- Focus on financial inclusion

Importance of the Banking System in Pakistan

The banking system is crucial for Pakistan’s economic functioning because it:

- Mobilizes public savings

- Provides loans to businesses and individuals

- Supports trade and industrial growth

- Facilitates government financial operations

- Promotes financial inclusion

Without a stable banking system, economic development would be difficult to sustain.

Structure of the Banking System in Pakistan

Pakistan’s banking system can be broadly divided into the following categories:

- Central Bank

- Commercial Banks

- Islamic Banks

- Development Finance Institutions

- Microfinance Banks

Each category has a specific role in the financial ecosystem.

Role of the Central Bank: State Bank of Pakistan (SBP)

The State Bank of Pakistan (SBP) is the central bank of the country and the backbone of the banking system.

Key Functions of SBP

- Issuing currency

- Formulating and implementing monetary policy

- Regulating and supervising banks

- Managing foreign exchange reserves

- Ensuring financial stability

SBP plays a critical role in controlling inflation and maintaining confidence in the banking system.

Commercial Banks in Pakistan

Commercial banks form the largest segment of the banking system.

Key Features

- Operate on a profit basis

- Serve individuals, businesses, and corporations

- Offer a wide range of banking services

Services Provided

- Savings and current accounts

- Fixed deposits

- Personal and business loans

- Credit cards

- Trade finance

Commercial banks are widely used for everyday banking needs.

Islamic Banking in Pakistan

Islamic banking has grown rapidly in Pakistan due to strong demand for Shariah-compliant financial services.

Core Principles

- No interest (riba)

- Profit-and-loss sharing

- Asset-backed financing

Islamic Banking Products

- Islamic savings accounts

- Murabaha and Ijarah financing

- Islamic home and auto finance

Islamic banks operate under SBP supervision and follow Islamic finance principles.

Development Finance Institutions (DFIs)

Development Finance Institutions are designed to support long-term economic development.

Key Objectives

- Financing large-scale projects

- Supporting industrial growth

- Providing long-term loans

DFIs play a role in sectors such as infrastructure, energy, and agriculture.

Microfinance Banks

Microfinance banks focus on providing financial services to low-income individuals and small entrepreneurs.

Services Offered

- Small loans

- Micro-savings accounts

- Micro-insurance products

These banks support poverty reduction and entrepreneurship.

Banking Services for Individuals

Banks in Pakistan offer various services to individual customers.

Common Services

- Savings accounts

- Current accounts

- Fixed and recurring deposits

- Personal loans

- ATM and debit card services

Digital banking has made these services more accessible.

Banking Services for Businesses

Businesses rely heavily on banks for daily operations and growth.

Business Banking Services

- Business accounts

- Working capital loans

- Trade finance

- Payment and payroll solutions

Small and medium enterprises (SMEs) benefit significantly from bank financing.

Digital and Branchless Banking in Pakistan

Technology has transformed banking services across the country.

Key Developments

- Mobile banking apps

- Internet banking

- Branchless banking agents

- Mobile wallets

Digital banking has expanded access to financial services, especially in remote areas.

Regulation and Supervision of Banks

The banking system in Pakistan is strictly regulated.

Regulatory Authority

- State Bank of Pakistan (SBP)

SBP ensures:

- Capital adequacy

- Risk management

- Consumer protection

- Compliance with banking laws

Strong regulation helps maintain system stability.

Deposit Protection in Pakistan

Pakistan has a deposit protection mechanism to safeguard depositors.

Key Points

- Protects eligible deposits up to a specified limit

- Applies to commercial and Islamic banks

- Enhances public trust

Deposit protection increases confidence in the banking system.

Role of Banks in Economic Development

Banks contribute to Pakistan’s development by:

- Financing industries and businesses

- Supporting agriculture and SMEs

- Promoting savings and investment

- Facilitating international trade

A healthy banking sector supports long-term economic growth.

Challenges Facing the Banking System in Pakistan

Despite progress, the banking system faces challenges.

Key Challenges

- Non-performing loans

- Economic instability

- Inflation and interest rate fluctuations

- Cybersecurity risks

Banks and regulators continue to address these issues through reforms and innovation.

Advantages of the Banking System in Pakistan

- Strong central bank oversight

- Growing Islamic banking sector

- Expanding digital banking

- Increasing financial inclusion

These strengths support resilience and growth.

Banking System in Pakistan vs Other Countries

Compared to many developing countries, Pakistan’s banking system is:

- Well-regulated

- Diversified

- Increasingly digital

However, further reforms are needed to improve efficiency and access.

Importance of Financial Inclusion

Financial inclusion is a key goal of Pakistan’s banking system.

Benefits

- Access to savings and credit

- Support for small businesses

- Reduction in cash-based transactions

Banks play a central role in inclusive growth.

Frequently Asked Questions (FAQs)

Who regulates banks in Pakistan?

Banks are regulated by the State Bank of Pakistan.

Is Islamic banking popular in Pakistan?

Yes, Islamic banking is growing rapidly.

Are bank deposits safe in Pakistan?

Deposits are protected under a deposit protection scheme.

Can foreigners open bank accounts in Pakistan?

Yes, subject to identification and regulatory requirements.

Conclusion

The banking system in Pakistan is a crucial pillar of the country’s financial and economic structure. With a strong central bank, diverse types of banks, and growing digital services, the system supports individuals, businesses, and national development. While challenges such as economic volatility and cybersecurity risks remain, ongoing reforms and technological advancements continue to strengthen the sector.

Understanding how the banking system in Pakistan works provides valuable insight into the country’s financial landscape and its role in economic progress.

Disclaimer

This article is for informational and educational purposes only. Banking regulations and services may change over time. Always refer to official bank or regulatory sources for the latest information.