Introduction

A credit score is one of the most important numbers in your financial life, yet many people do not fully understand what it means or why it matters. Whether you are applying for a loan, a credit card, or even a rental home, your credit score plays a major role in the decision-making process.

A good credit score can help you get loans easily, enjoy lower interest rates, and build long-term financial stability. On the other hand, a poor credit score can limit your options and increase borrowing costs. This guide explains what a credit score is, how it is calculated, and why it matters, using simple language suitable for beginners.

What Is a Credit Score?

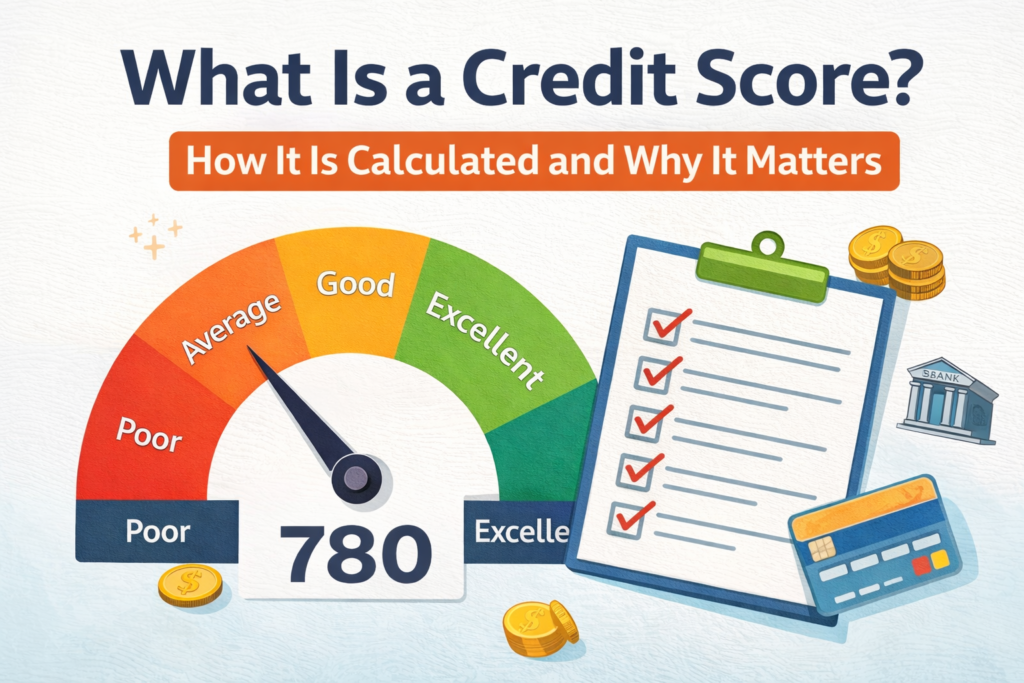

A credit score is a numerical value that represents your creditworthiness. It shows lenders how responsibly you have managed credit in the past. In simple terms, it helps banks and financial institutions decide whether they should lend money to you and under what terms.

Credit scores are usually based on your credit history, including loans, credit cards, and repayment behavior. The score reflects how likely you are to repay borrowed money on time.

Credit Score Range Explained

Most credit scores fall within a specific range. While exact ranges may vary slightly, a general understanding looks like this:

- Excellent score: Very strong credit profile

- Good score: Reliable borrower

- Average score: Acceptable but needs improvement

- Poor score: High risk for lenders

A higher score indicates better credit discipline and financial responsibility.

Why Credit Score Is Important

Your credit score impacts many areas of your financial life. It is not just about loans.

Key Benefits of a Good Credit Score

- Easier loan approvals

- Lower interest rates

- Higher credit limits

- Better credit card offers

- Faster processing of applications

A strong credit score can save you money in the long run by reducing interest and fees.

How Is a Credit Score Calculated?

A credit score is calculated using several factors related to your credit behavior. Each factor contributes differently to the final score.

Payment History

Payment history is one of the most important factors. It includes:

- On-time payments

- Late payments

- Missed payments

Paying bills on time consistently helps maintain a healthy credit score.

Credit Utilization

Credit utilization refers to how much credit you use compared to your total available credit.

For example:

- Low usage shows responsible credit management

- High usage may indicate financial stress

Keeping credit usage under control positively impacts your score.

Length of Credit History

This factor looks at how long you have been using credit.

- Older credit accounts improve score stability

- Longer credit history builds trust with lenders

Maintaining old accounts responsibly can be beneficial.

Credit Mix

Credit mix refers to the types of credit you use, such as:

- Credit cards

- Personal loans

- Home loans

- Education loans

A balanced mix shows you can manage different types of credit responsibly.

New Credit Applications

Every time you apply for new credit, it may temporarily affect your score.

- Multiple applications in a short period can reduce your score

- Responsible and limited applications are better

Apply for credit only when necessary.

How Often Does Credit Score Change?

Your credit score is not fixed. It changes based on your financial behavior.

Actions that can change your score:

- Paying bills on time

- Missing payments

- Using more or less credit

- Opening or closing accounts

Regular monitoring helps you stay aware of your credit health.

Common Myths About Credit Scores

There are many misconceptions surrounding credit scores.

Myth 1: Checking Your Score Reduces It

Checking your own credit score does not harm it. Regular checks help you track progress.

Myth 2: Income Affects Credit Score

Your income does not directly impact your credit score. Credit behavior matters more.

Myth 3: No Credit Means Good Credit

Having no credit history makes it harder for lenders to assess you.

How to Improve Your Credit Score

Improving a credit score takes time and consistency.

Practical Tips

- Pay all dues on time

- Keep credit card usage low

- Avoid unnecessary loans

- Maintain older credit accounts

- Review credit reports regularly

Small improvements done consistently can lead to strong results.

Credit Score and Loans

When you apply for loans, your credit score influences:

- Approval chances

- Interest rates

- Loan amount

- Repayment terms

A higher score often results in better loan offers and lower costs.

Credit Score and Credit Cards

Credit card issuers rely heavily on credit scores.

With a good score, you may receive:

- Higher credit limits

- Lower interest rates

- Better reward programs

Responsible credit card usage helps maintain a strong score.

Importance of Monitoring Your Credit Score

Monitoring your credit score helps you:

- Detect errors early

- Prevent identity-related issues

- Track financial progress

Checking your score periodically is a good financial habit.

FAQs About Credit Scores

What is a good credit score?

A good credit score generally reflects responsible borrowing and timely repayments.

How long does it take to improve a credit score?

Improvement depends on behavior. Consistency over months shows results.

Can one missed payment affect my score?

Yes, missed payments can negatively impact your credit score.

Conclusion

A credit score is a key indicator of your financial reliability. Understanding how it works and what affects it can help you make smarter financial decisions. By paying bills on time, managing credit responsibly, and avoiding unnecessary debt, you can build and maintain a strong credit score over time.

A good credit score is not built overnight, but with discipline and awareness, it becomes a powerful tool for long-term financial stability.

Disclaimer

This article is for educational purposes only and does not provide financial or credit advice. Always review your personal financial situation before making decisions.